Welcome to my new weekly fintech focused column. I have been publishing this every Sunday but on March 27, this column turns into a newsletter! So, if you want to have it hit your inbox directly starting then, sign up here.

2021 was a record year for venture capital fundraising, and fintechs were the largest recipients of funding worldwide, with about 21% of all venture dollars last year going into fintech startups.

We all knew – or at least some of us did, ahem – that this was likely not sustainable in the long term. Investors appeared to be backing some startups in part due to FOMO, and that’s not necessarily a good thing.

So as the first quarter draws to a close, it’s clear that while in no way have fundraises come to a screeching halt, investors are starting to pump the brakes. Generally, it appears we are experiencing a market pullback – which Alex touches on in this piece – precipitated by a number of things, not the least of which – the conflict in Ukraine and disappointing performances by companies who went public in the last year. And fintech, last year’s rising star of venture, is not immune.

My former colleague, Joanna Glasner, at Crunchbase News published a story on March 7 indicating that venture capitalists’ enthusiasm for fintech seems to be waning as of late. Her data point, according to Crunchbase data, was that in the two weeks leading up to her post, a total of 51 fintech companies across the globe collectively had raised $1.1 billion in seed through late-stage venture funding. That was down about 63% from the prior two-week period, during which 80 companies raised just shy of $3 billion.

Last year, it was truly a founders’ market, meaning that terms were more founder-friendly than ever. Many buzzy startups had their pick of investors and found themselves presented with multiple term sheets. In many cases, companies were raising money left and right at very early stages, with little more than a deck, idea and team established.

One founder of a very fast-growing fintech startup in particular, who I cannot yet name until his company’s upcoming round is announced (stay tuned), told me Friday that when raising for a round in early 2022, he saw a big difference in the “level of diligence” on the part of investors than he saw in 2021.

“Last year, even for us, it was like, ‘look at this pretty graph, we’re growing so quickly,’ ” he recalls. “And everyone was like, ‘yeah, that makes sense, let’s invest in this.’ ”

This year, on the other hand, there were more questions about margins, operations, revenue coming in – what the contribution was like on each, he added.

“We went through the whole gauntlet in January and February,” he told me. “That’s why, honestly, this raise feels very satisfying.”

In talking with other founders, he realized that they were experiencing similar things.

“It’s an absolutely different environment from Q4 of last year,” he said, “not just in terms of the level of diligence but also, in the access to capital. While there is still a lot of dry powder, it’s not as easy to get it on the specific terms you want to get it as it used to be.”

And in his view, and mine quite frankly, that’s not a bad thing.

Founders having to provide tangible evidence of a valid business model with real numbers makes more sense than, as he put it, “Hey, look at these pretty things. Give me a check for that.”

Not to keep tooting our own horn, but the Equity team late last year predicted this would happen. Selfishly, for the sake of my inbox (and sanity!), I am all for investors being more discriminating when it comes to which companies they decide to back. And for the founders who are able to raise in a more challenging environment, it should also – as in the case of the aforementioned founder – feel more rewarding when they do close on those fundraises.

Note: Of course in this crazy startup world, things change week by week, and my friend and fellow fintech enthusiast Nik Milanovic shared in his own newsletter on Saturday that “52 (52!) fintech companies raised $2.76 billion. A record for the number of funding rounds and close to the record for most funding raised by fintech in a single week.” I’m waiting to see what first quarter numbers look like or even better, second quarter numbers. There’s always a lag so fundings being announced now have likely been in the works for a little while.

Oops, Better.com did it again

I am as weary of writing about Better.com as you probably are of reading about it. But I would be remiss not to include mention of the events of the last week, which included my breaking the news about the company’s mass layoff of about 3,000 people. Astonishingly, after a fiasco of a December layoff that affected 900 people, the digital mortgage lender managed to botch things again. Affected employees shared that they found out that they were getting laid off when a severance check randomly appeared in their payroll app, and then was mysteriously removed. Long story short, the company had planned to conduct the layoffs one on date, changed their minds presumably due to a leak and then forgot to update the timing of when the severance checks would go out. It was a mistake that might have been forgiven if the company had not royally screwed up its December mass layoff by conducting it coldly during a Zoom call.

I would like to make clear that as any competitive reporter, I love getting scoops as much as the next journalist. However, scoops on mass layoffs are by far the least fun to get. It sucks that so many people have lost their jobs at this company in the past few months. And while market conditions (rising interest rates that have led to fewer re-financings, among other things) surely played a factor in the decision, it would be foolish not to surmise that the severe hit to its reputation has to be impacting Better.com’s ability to win new customers seeking to purchase homes and thus, its overall business.

Bottom line: at some point, any company may have to lay off employees. But there is a big difference in handling it with compassion and respect than in handling it in a way that offends not only the employees themselves, but even casual observers. And for proof of the latter point, one need need look no further than the comments on my posts on LinkedIn and Twitter.

After I wrote all of the above, I came across a LinkedIn post from a Better.com employee who on March 11 was asked to resign a week early after publishing an internal communication from the company on social media. Senior product designer Eric Blattberg publicly pushed his employer — including direct communications with CEO Vishal Garg and CFO Kevin Ryan on LinkedIn and Slack — to provide additional severance pay and extended insurance benefits to the expecting parents who were being laid off. The company reportedly pledged to offer these employees extended COBRA benefits for 12 months.

Image Credits: Eric Blattberg

His experience illustrates Better’s efforts to make itself look better (he was asked personally by Garg to post the company’s efforts on social media), the disappointment that many of its former employees feel and what accountability looks like. At least Better — in this case — pledged to do the right thing. Until it didn’t?

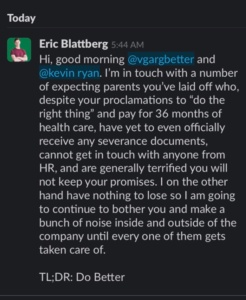

As of March 12, there were reports of the extended benefits not amounting to 12 months as promised. According to Blattberg, who posted the following on LinkedIn:

Better is adding to its string of corporate incompetence today with written agreements to expecting parents that differ from what a Better lawyer reading from a script promised them in a phone call, according to two of the expecting parents who noted the disparities to me earlier today. In the phone call with the laid-off employees, the Better lawyer promised four additional weeks of severance pay and 12 additional months of paid COBRA premiums on top of the standard package offered to all laid-off employees, bringing their health insurance coverage to the end of June 2023, the expecting parents told me. But in an email subsequently received by the expecting parents, the COBRA coverage was only nine additional months, bringing their coverage to March 2023, and there was no additional severance pay offered. In a subsequent communication with one of the expecting parents described to me this morning, the lawyer admitted to making a mistake, confusing the 20 days of extended severance offered to all fired employees as additional pay in their custom package, but declined to honor the prior commitment. This is, as usual, unacceptable. Better should #DoBetter.

I reached out to Better.com and a spokesperson sent me a link to the original letter sent to employees on March 8 but declined to respond to any questions regarding health insurance benefits, citing privacy concerns.

Via DMs, Eric told me: “On Tuesday morning I found myself in a unique position of privilege: still inside Better as it casually fumbled the layoffs it had spent months planning, causing an unfathomable amount of collateral damage, but not scared of losing my job, since I was sitting on an offer from Ergatta, where I’ll start as a senior product designer March 21… My only goal this whole time has been to help people. I don’t want to tear the company down, I want to shield the employees Vishal has tossed aside like they were just numbers on a balance sheet. They are not just a number. Every one of them has their own story, their own health care journey, their own reason for working at Better. And they deserve so much more respect, consideration, and support than they received this week. So I’m going to keep fighting on their behalf from the outside.”

SPAC is a four-letter word

On EquityPod this week, Alex, Natasha and I dug into the increasing number of companies ditching their SPACs and opting to raise money instead with the latest example being Acorn, which this week announced it raised $300M at a nearly $2B valuation – in line with what it would have raised in the SPAC anyway. Companies like Acorn and Kin Insurance are doing this for a variety of reasons, including a currently unfavorable public market. But also, I think companies (and investors) are realizing what some of us already suspected – that anything that is too easy to come by is probably not worth having. Case in point: Acorn’s CEO Noah Kerner told me that when Acorn does decide to go public, it will be via the traditional IPO route. Thus, we concluded that SPAC is a four-letter word, again.

LatAm and Africa’s maturing startup scenes

Latin America raised a record amount of venture capital last year and now we’re seeing more signs of an increasingly maturing market. This week alone, I wrote about two companies that were co-founded by the founders of unicorns in the region. The first was Mara, a a São Paulo-based startup that aims to “reinvent” the grocery shopping experience for the underserved in Latin America. One of its co-founders is Ariel Lambrecht, who also helped start mobility startup 99, Brazil’s first unicorn. The second was Yuno, a two-month-old Colombian payments startup which raised $10 million in a seed round of funding co-led by a16z, Kaszek and monashees.

Image Credits: Co-founders Juan Pablo Ortega and Julian Nunez / Yuno

The ability to raise a relatively large seed round so soon after inception speaks to the experience of the company’s founders, which include Juan Pablo Ortega, the co-founder of on-demand delivery unicorn Rappi (which as of last July was valued at $5.25 billion) and Julián Núñez, an early Rappi employee.

As Latin America’s startup ecosystem continues to grow, there is no doubt we will only see more founders of successful companies go on to start new ones and invest in other early-stage startups in which they see potential.

There are many parallels between LatAm and Africa, which is also seeing its startup scene grow impressively. Some of us who have been paying attention view Africa at a place currently where LatAm was a few years ago, just starting to attract more global interest and dollars – especially in fintech startups.

In December 2021, Uganda’s multi-service and digital payment technology platform SafeBoda became the first startup on the continent to receive investment from the Google fund. It has now been joined by fintech Numida, which emerged as the first startup in the country to get into YC (W22). And damn, out of Ghana this past week, Dash raised a $32.8 million seed round (enormous by even U.S. standards) led by Insight Partners, a New York-based private equity and venture capital firm, to build “a connected wallet for Africans.”

There is a certain energy coming out of LatAm and Africa that is refreshing and exciting to cover and I can’t wait to see what’s next in both regions.

Image Credits: Dash

Fundings

Honestly, even I was impressed with the number of global fintech-related fundings published on TechCrunch over the past week – a testament to the kick-ass team of reporters we have all over the world.

I can’t include all the cool fintech funding deals that took place this last week so I’m going to narrow it down to a few from each continent along with some others that were announced that TC didn’t cover for one reason or another.

Indian fintech CredAvenue turns unicorn with fresh $137 million funding

Crypto mortgage lender Milo secures $17 million investment

Roofstock valued at $1.9 billion with new funding round led by SoftBank Vision Fund 2

US paytech Stax hits $1bn valuation with $245m funding round

Propel raises $50m Series B to help Americans with low income make it through the month, every month

CoFi closes on $7 million seed to transform construction financing

Colombia’s Acasa, a “buy before you sell” financing solution has US$38 million in fresh funds for those who want to move house Note: Acasa is apparently the first “Buy Before You Sell” proptech company in LatAm (like Knock, Orchard, Fly Homes and Homeward in the U.S.).

Argyle raises $55M Series B to “make fair credit decisioning possible for every lender and consumer through real-time, user-permissioned access to employment data”

Capchase closed an $80 million Series B as the company looks to expand its funding platform that offers founders non-dilutive financing alternatives. The new round was led by 01 Advisors.

In other news

Zeta, a SoftBank-backed provider of next-gen credit card processing to banks and fintechs which became a unicorn last May, and Mastercard on March 7 announced a 5-year global partnership. As part of the agreement, the companies said they will go-to-market jointly to launch credit cards with issuers worldwide on Zeta’s “modern, cloud-native, and fully API-ready credit processing stack.” Mastercard also invested in the company as part of a $30 million raise that took the company to a $1.45B valuation, according to the Economic Times.

TripActions, which was focused on travel but has since expanded into corporate spend and expense management, gave me a sneak peek at the launch of its new offering, Auto-Itemization, which t says leverages artificial intelligence and machine learning “to automatically assign individual line items on a receipt to expense categories and then applies company policy to each line item.” This move is yet another example of how the corporate spend space is getting increasingly competitive. I also wrote this past week about a new startup called Glean AI, which describes itself as “accounts payable with a brain.”

Numerous tech companies have joined the growing list of tech brands that are suspending their operations in Russia amid its invasion of Ukraine. The latest batch of companies doing so includes several notable names, including financial services companies such as PayPal, Mastercard, Visa and more.

Airtel said on March 7 it is launching a credit card, the latest attempt from the Google-backed Indian telecom operator to make inroads with financial services as it looks to expand its offerings in the world’s second-largest internet market.

Klarna’s earnings tell us, writes Alex, that the BNPL market continues to expand, with consumers happy to transact more and more with the spending model. They also show us that growth in BNPL land is not cheap; Klarna’s operating costs are scaling rapidly and the company’s profitability is suffering.

On March 9, Public announced that it had purchased Otis, a startup that allows consumers to buy and trade fractional shares in individual alternative assets.

Portage Ventures announced the $616M close of its third fund, which it claims to be one of the largest early-stage fintech funds worldwide.

Jerry jumped into the auto loan refi space. We covered the startup’s last raise – a $75M round at a $450M valuation – last August.

And last but not least, I wrote about how Credit Karma, Betterment and Austin-based startup Chipper want to provide student loan borrowers with some relief options.

Well, that’s it for this week. Please note that I’ll be out next week, enjoying spring break with my family so there will be no column published on March 20. But my newsletter formally launches on March 27 so if you haven’t subscribed yet, now is the time!

Take care and be safe!