FPL Technologies, an Indian startup that offers credit cards to customers under the brand name OneCard, is the latest in the South Asian market to join the unicorn club following a new round of funding.

Singapore’s Temasek, one of the world’s largest investors, led the Pune-headquartered startup’s Series D round of over $100 million, OneCard disclosed in a filing to the local regulator. The new round values OneCard at over $1.4 billion (post-money), up from about $750 million in January this year, a source familiar with the matter told TechCrunch.

Existing backers QED, Sequoia Capital India and Hummingbird Ventures were among those who participated in the new round, which brings OneCard’s to-date raise to over $225 million.

OneCard declined to comment Wednesday evening. TechCrunch reported in February that Temasek was in talks to lead a round of over $100 million in OneCard at a valuation of about $1.5 billion. Indian news outlet Entrackr first reported about the filing.

Fewer than 30 million Indians have a credit card today, which has created a huge whitespace for startups in the country to innovate on tech and reach more consumers. Banks in the country, and beyond, are increasingly attempting to expand their own credit card customers bases, but their stringent and archaic eligibility criteria make most Indians unworthy of credit cards.

And that’s a factor that OneCard founders understand very deeply.

Founded by banking veterans in 2019, OneCard operates a mobile-first credit card. Its cards, for which the startup partners with banks, come without any joining or annual fee and give customers more control and flexibility over how and where they transact. It also offers a range of personalised rewards and loans to customers.

The startup also operates an app called OneScore, which helps users understand and learn their credit score. The app is one of the largest customer acquisition drivers for OneCard, it has said previously.

OneCard said earlier this year that it had amassed over 250,000 customers who were spending about $60 million with its cards each month. Anurag Sinha, the startup’s co-founder and chief executive, said in January that he estimated that about 80 million to 90 million Indians were eligible to have a credit card.

That’s not to say that credit card companies are not facing some of their own challenges. UPI, a five-year-old payments rail developed by retail banks, has quickly gained adoption and is the most popular way Indians transact today. The fast inroads of UPI has eroded some usage of debit cards, though it appears credit cards are so far largely immune from it.

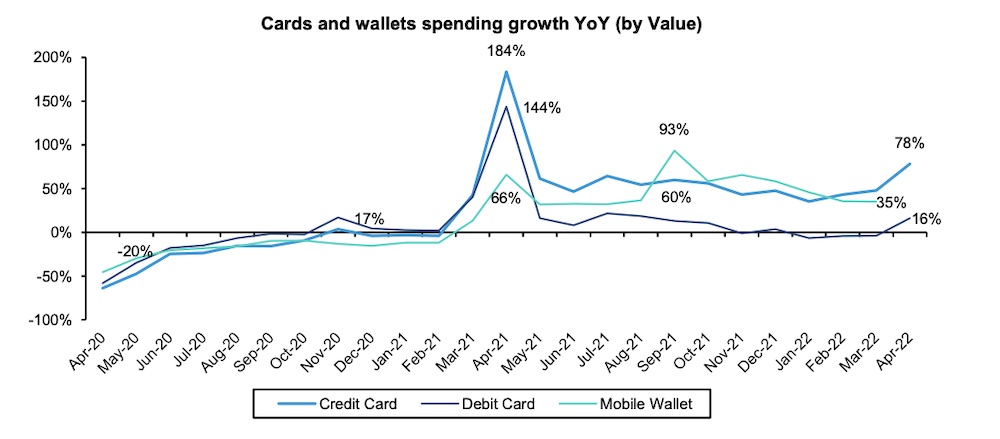

Data: NPCI, RBI, Bernstein analysis. Image: Bernstein.

“UPI P2M transaction value exceeded total credit and debit card spending for the fourth month running. The share of P2M transactions was up from 16.6% to 18% YoY in value. Wallets are picking up traction again (+35% YoY, by value). We think the bounce-back comes from Paylater fintechs disbursing credit through the wallet/PPI route,” wrote a Bernstein analyst in a note to clients last month.

“We think this will continue to impact debit cards and credit cards (albeit to a lesser extent). Credit card spending growth was +78% YoY, with debit card spending growth at +16% YoY. We think the mobile over cards, and credit over debit theme poses a big threat to debit cards (spend growth), and to credit cards (albeit to a lesser extent — spend growth, pricing pressures),” it added.

Moreover, the central bank’s recent directive that the role of co-branding partner for credit cards should be limited to marketing and distribution of cards and providing acess to the cardholder for the goods and services that are offered is expected to hurt many credit card startups.

The central bank’s another recent move of integrating credit cards with UPI is expected to drive higher spending on credit cards but it poses a threat to their business model as “there is limited clarity on the merchant discount rate (MDR) for such payments,” the analyst wrote.