Pensions, by just about any estimation, are a good thing. Ever since the U.K. government introduced auto-enrolment to the national workforce back in 2012, forcing employers to provide a workplace pension scheme by default (i.e. opt-out), this has led to more people saving toward their retirement.

This policy change, however, means that millions of people around the country now have multiple different pension funds with different providers. Given that the average worker only remains in the same job for a few years, when they move to a new employer, a new pension fund automatically begins — quite probably with a completely different provider to their previous one — which creates this giant fragmented pension palaver.

Some of the more organized workers out there will no doubt “consolidate” their own pensions as their career evolves, but for many it’s too big an administrative headache when all they really want to do is focus on their new job. This is a problem that fledgling U.K. fintech startup Penny is trying to solve, with an AI-powered platform that automatically consolidates users’ pension funds under a single roof.

“The average, hard-working person doesn’t have a clue who their pension provider is, let alone who their past employers used as their pension providers,” Penny cofounder and CEO Josh Stott explained to TechCrunch. “Quite quickly, you have most of your net worth scattered around various pension providers. Do you think the pension providers care? Or do you think they’re happy to keep charging fees on your old pension pot?”

Founded out of Bristol in 2019, Penny is now a remote-first startup with employees based around the U.K. The company launched to market roughly a year ago, and claims to have helped “thousands of British customers locate and consolidate” all their current and historical pension funds, amounting to more than £50 million ($60 million).

To fund the next phase of its growth, Penny today announced it has raised £4 million ($4.8 million) in seed funding from Google’s Gradient Ventures, with participation from a handful of notable figures in the fintech world, including Monzo founder Tom Blomfield and Payhawk cofounder and CEO Hristo Borisov.

The funding values Penny at £25 million ($30 million).

Penny CEO Josh Stott (center) flanked by cofounders Ben Stokes (left) and Nate Stott

How it works

Through the Penny mobile app, available on Android and iOS, users are asked a few questions, such as their name, mobile number, date-of-birth, address, national insurance number, and previous jobs, and Penny takes care of the rest.

It’s worth noting that Penny factors in the reality that most people probably don’t have any information relating to their old pensions, such as their policy numbers — and this is one of the key differentiators it touts over the more established incumbents in the space such as PensionBee (which became a publicly-traded company last year). Penny strives to do most of the painful leg-work for them.

“We knew that to serve the mass market individual, we’d need to be able to find customers’ pension information for them, using information they already know,” Stott explained. “Penny’s ability to automatically find pension information for a customer is what has allowed us to onboard lower-value but extremely numerous customers.”

To do this, Penny leans on good old-fashioned AI to plow through myriad pension data sources — some publicly available, some private — most of which is housed in dusty PDF format. These digital documents often contain incomplete or long out-of-date information, prepared by different people and organizations who adhered to different formatting and language, making the whole thing hugely inconsistent. And that is why Penny uses natural language processing (NLP) to automate the process of finding users’ old pension details — it would be too time-consuming to do this by any other means.

“We harness NLP to detect and extract the correct data for our customers, and to provide information on their pension policies,” Stott explained. “Without NLP, we simply wouldn’t be able to process the amount of data we need to find pensions.”

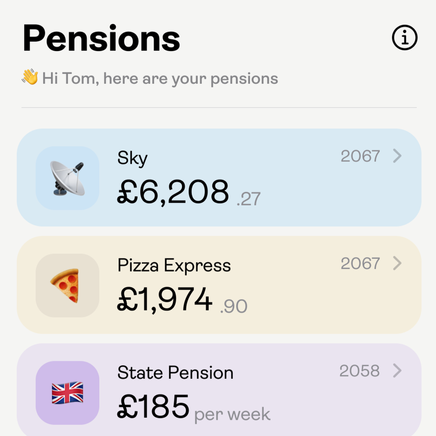

Although Penny is very much about consolidating pensions, an interesting quirk with the app is that it continues to display each pension separately rather than as a single entity. It turns out there is a good reason for that — it’s all about how end-users think about their pensions.

“In user testing, we found that people intuitively connect their pensions to their jobs, rather than to nameless pension schemes,” Stott explained. “When we displayed multiple pensions as a single figure, it actually created a negative experience for many customers. So, although Penny consolidates pensions into a new pension fund, we keep them as separate pots within the fund for a better user experience.”

Penny app

A pretty penny

None of this comes for free, of course, but then managing pension funds is never a gratis endeavor. All pension companies charge a fee for managing funds, and those fees obviously multiply the more separate pensions a person has. So when Penny consolidates pensions into its own plan (which is managed by HSBC), those various fees stop and customers instead pay a single annual charge of 0.75% of the pension’s value.

For the foreseeable future, Penny remains focused entirely on the U.K. market, which is understandable given that it represents the second biggest pensions market globally after the U.S. Moreover, untouched pension wealth in the U.K. was pegged at almost £300 billion in 2018 (not all of this is forgotten pension pots though — some people simply want to let their investments accrue). But some U.S. states, such as California, are starting to adopt auto-enrolment pension regulations too, which could open the door for Penny to extend its reach into new locales.

“We plan to launch in California in the next few years, but currently have a singular focus on our own domestic market,” Stott said.

In the nearer term, Penny plans to introduce more features to the app, including the ability to trade stocks directly from pension pots, and eventually crypto too.

All this leads us back to the main thrust of today’s news, vis-à-vis one of Google’s venture capital arms leading a £4 million investment into Penny. So how did all of this come about, exactly? It turns out a prominent figure from the fintech world stumbled up on Penny and wrote about it in their newsletter, which was then picked up by someone at Gradient, who then reached out to Stott.

“We got on well, they understood the product and our ambitions,” Stott explained. “From that point on, I added them to my monthly investor updates — it seemed the simplest way of letting them really know what was going on at Penny. Before we went to market to raise a seed round, Gradient approached us and asked to lead.”

While AI is no longer the singular focus for Gradient Ventures that it was at the fund’s launch five years ago, it still plays a significant part in its investment philosophy, which will have positioned Penny favorably. But as with just about any investment, the most important factor is the size of the addressable market.

“At Gradient, we fund great teams and products in massive markets,” Gradient Ventures’ general partner Darian Shirazi said in a statement. “The pension market is trillions of dollars worldwide, and accessing these funds is cumbersome for all savers and especially for retirees.”